Page 183 - EXIM-Bank_Annual-Report-2023

P. 183

Management Discussion and Analysis Ensuring Sustainability Commitment to Lead Upholding Accountability Financial Statements 181

Notes to the fiNaNcial statemeNts

43. FINANCIAL rISk MANAGEMENT PoLICIES (cont’d)

Capital management (cont’d)

Regulatory capital

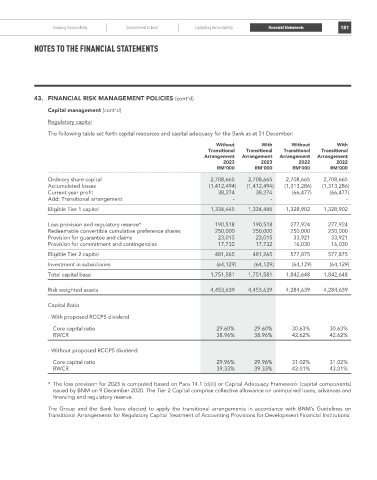

The following table set forth capital resources and capital adequacy for the Bank as at 31 December:

Without With Without With

Transitional Transitional Transitional Transitional

Arrangement Arrangement Arrangement Arrangement

2023 2023 2022 2022

rM’000 rM’000 rM’000 rM’000

Ordinary share capital 2,708,665 2,708,665 2,708,665 2,708,665

Accumulated losses (1,412,494) (1,412,494) (1,313,286) (1,313,286)

Current year profit 38,274 38,274 (66,477) (66,477)

Add: Transitional arrangement - - - -

Eligible Tier 1 capital 1,334,445 1,334,445 1,328,902 1,328,902

Loss provision and regulatory reserve* 190,518 190,518 277,924 277,924

Redeemable convertible cumulative preference shares 250,000 250,000 250,000 250,000

Provision for guarantee and claims 23,015 23,015 33,921 33,921

Provision for commitment and contingencies 17,732 17,732 16,030 16,030

Eligible Tier 2 capital 481,265 481,265 577,875 577,875

Investment in subsidiaries (64,129) (64,129) (64,129) (64,129)

Total capital base 1,751,581 1,751,581 1,842,648 1,842,648

Risk weighted assets 4,453,639 4,453,639 4,284,639 4,284,639

Capital Ratio

- With proposed RCCPS dividend

Core capital ratio 29.60% 29.60% 30.63% 30.63%

RWCR 38.96% 38.96% 42.62% 42.62%

- Without proposed RCCPS dividend

Core capital ratio 29.96% 29.96% 31.02% 31.02%

RWCR 39.33% 39.33% 43.01% 43.01%

* The loss provision for 2023 is computed based on Para 14.1 (d)(ii) or Capital Adequacy Framework (capital components)

issued by BNM on 9 December 2020. The Tier 2 Capital comprise collective allowance on unimpaired loans, advances and

financing and regulatory reserve.

The Group and the Bank have elected to apply the transitional arrangements in accordance with BNM’s Guidelines on

Transitional Arrangements for Regulatory Capital Treatment of Accounting Provisions for Development Financial Institutions.