Page 221 - EXIM-Bank_Annual-Report-2023

P. 221

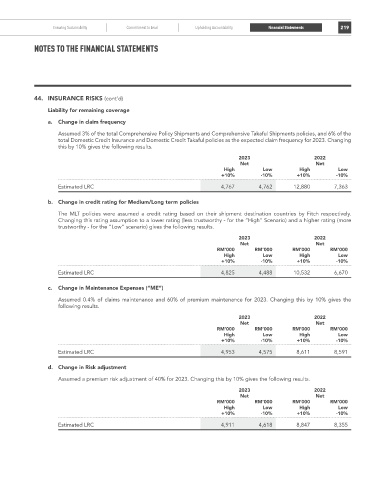

Management Discussion and Analysis Ensuring Sustainability Commitment to Lead Upholding Accountability Financial Statements 219

Notes to the fiNaNcial statemeNts

44. INSurANCE rISkS (cont’d)

Liability for remaining coverage

a. Change in claim frequency

Assumed 3% of the total Comprehensive Policy Shipments and Comprehensive Takaful Shipments policies, and 6% of the

total Domestic Credit Insurance and Domestic Credit Takaful policies as the expected claim frequency for 2023. Changing

this by 10% gives the following results.

2023 2022

Net Net

high Low high Low

+10% -10% +10% -10%

Estimated LRC 4,767 4,762 12,880 7,363

b. Change in credit rating for Medium/Long term policies

The MLT policies were assumed a credit rating based on their shipment destination countries by Fitch respectively.

Changing this rating assumption to a lower rating (less trustworthy - for the “High” Scenario) and a higher rating (more

trustworthy - for the “Low” scenario) gives the following results.

2023 2022

Net Net

rM’000 rM’000 rM’000 rM’000

high Low high Low

+10% -10% +10% -10%

Estimated LRC 4,825 4,488 10,532 6,670

c. Change in Maintenance Expenses (“ME”)

Assumed 0.4% of claims maintenance and 60% of premium maintenance for 2023. Changing this by 10% gives the

following results.

2023 2022

Net Net

rM’000 rM’000 rM’000 rM’000

high Low high Low

+10% -10% +10% -10%

Estimated LRC 4,953 4,575 8,611 8,591

d. Change in Risk adjustment

Assumed a premium risk adjustment of 40% for 2023. Changing this by 10% gives the following results.

2023 2022

Net Net

rM’000 rM’000 rM’000 rM’000

high Low high Low

+10% -10% +10% -10%

Estimated LRC 4,911 4,618 8,847 8,355