Page 171 - EXIM-BANK-AR20

P. 171

Section 06 Financial Statements

169

42. FINANCIAL RISK MANAGEMENT POLICIES (CONT’D.)

Market risk management (cont’d.)

Measurement (cont’d.)

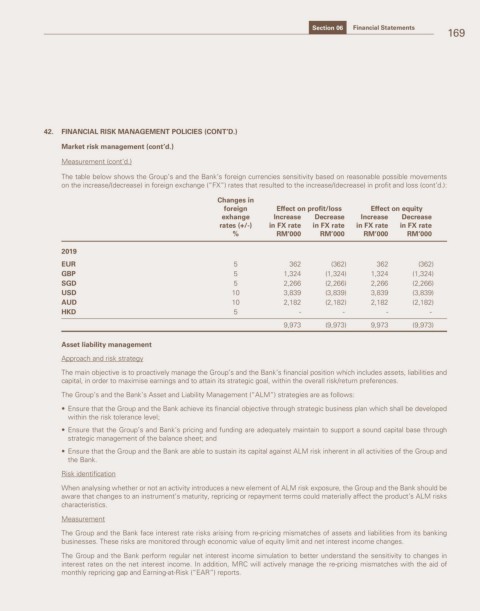

The table below shows the Group’s and the Bank’s foreign currencies sensitivity based on reasonable possible movements

on the increase/(decrease) in foreign exchange (“FX”) rates that resulted to the increase/(decrease) in profit and loss (cont’d.):

Changes in

foreign Effect on profit/loss Effect on equity

exhange Increase Decrease Increase Decrease

rates (+/-) in FX rate in FX rate in FX rate in FX rate

% RM’000 RM’000 RM’000 RM’000

2019

EUR 5 362 (362) 362 (362)

GBP 5 1,324 (1,324) 1,324 (1,324)

SGD 5 2,266 (2,266) 2,266 (2,266)

USD 10 3,839 (3,839) 3,839 (3,839)

AUD 10 2,182 (2,182) 2,182 (2,182)

HKD 5 - - - -

9,973 (9,973) 9,973 (9,973)

Asset liability management

Approach and risk strategy

The main objective is to proactively manage the Group’s and the Bank’s financial position which includes assets, liabilities and

capital, in order to maximise earnings and to attain its strategic goal, within the overall risk/return preferences.

The Group’s and the Bank’s Asset and Liability Management (“ALM”) strategies are as follows:

• Ensure that the Group and the Bank achieve its financial objective through strategic business plan which shall be developed

within the risk tolerance level;

• Ensure that the Group’s and Bank’s pricing and funding are adequately maintain to support a sound capital base through

strategic management of the balance sheet; and

• Ensure that the Group and the Bank are able to sustain its capital against ALM risk inherent in all activities of the Group and

the Bank.

Risk identification

When analysing whether or not an activity introduces a new element of ALM risk exposure, the Group and the Bank should be

aware that changes to an instrument’s maturity, repricing or repayment terms could materially affect the product’s ALM risks

characteristics.

Measurement

The Group and the Bank face interest rate risks arising from re-pricing mismatches of assets and liabilities from its banking

businesses. These risks are monitored through economic value of equity limit and net interest income changes.

The Group and the Bank perform regular net interest income simulation to better understand the sensitivity to changes in

interest rates on the net interest income. In addition, MRC will actively manage the re-pricing mismatches with the aid of

monthly repricing gap and Earning-at-Risk (“EAR”) reports.